Climate Tech is Dead...Long Live Climate Tech?

Has the Climate Tech investment bubble burst, does it need a re-brand, are investors spooked...and then the USA changed.

Is this the end of Climate Tech as we know it, or are we just onto the next cycle, or something else entirely - let's take a look.

Some Context

I started writing this a few weeks back as a review and recap on where we are in Climate Tech, once the end-of-year number crunching analysis arrived in January and February.

Then the barometer started to move, very quickly - the carnage that ensued in US climate policy was a feeding frenzy - impacting project deployment, pauses on I.R.A. funding and offshore wind licenses, the removal of people resources and data, defunding organisations such as NOAA, labelling and removing 'climate' as an offensive word across the Federal digital footprint - and so it goes, on and on, and on.

It's a tragedy that's still playing out via a shock-and-awe daily digest. In this article, we aren't recapping the last few weeks of US climate-related policy 'Executive Orders'. I have commented on those topics via the Newsletter and LinkedIn. Quite frankly with the daily dose, it's too much to jam into one post! 🤯

It has meant that I have started, stopped writing, started again, made revisions and deleted lots! This article is now through a different lens in light of the dramatic events of the US.

Have We Arrived?

Are we at the place where Climate Tech is ubiquitous, embedded into society, processes and industries? Where it's delivering function and purpose quietly in the background - mitigating climate breakdown, reducing emissions, slowing global temperature rises, and improving health, well-being and biodiversity.

Are we on track to meet our climate and sustainability goals, have we gamified climate change and "completed it"?

I think we can all agree we aren't at that place yet, and likely won't be for a very long time, if ever.

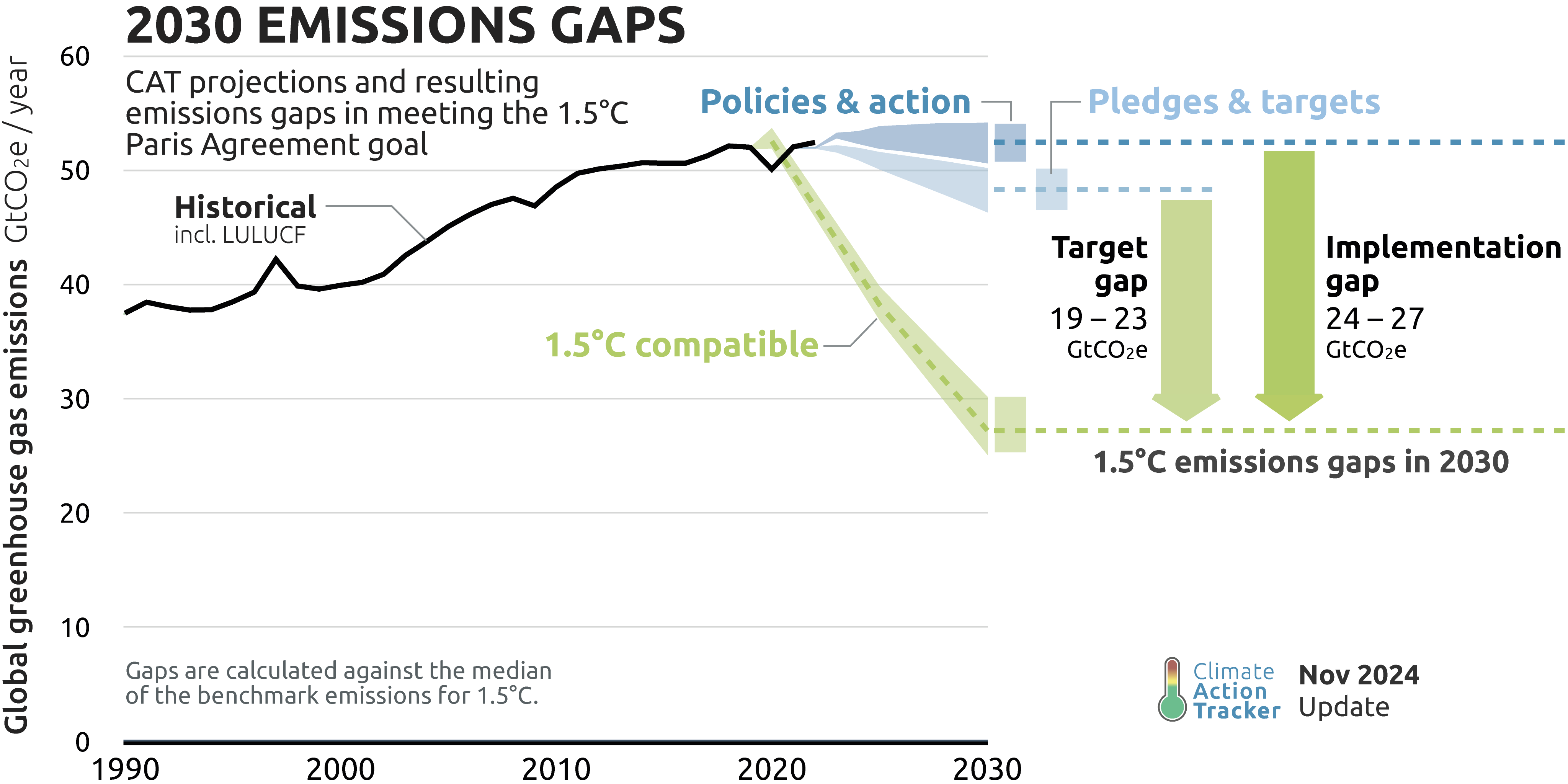

More in-depth insights on the emissions tracker from CAT here.

In my mind, until Climate Tech innovations are scaled globally, and we are a long way down the energy/transport/food/sustainability [add your own] transition, we still need Climate Tech innovation and deployment. Until mitigation and adaptation solutions are in equilibrium with, and embedded in society, it's very much needed.

We aren't there yet - so why are some people questioning Climate Tech as a 'thing' when it is desperately needed? The odds are we won't be able to hold below 2℃ warming, and probably even 3℃ - we need everything in the toolbox ASAP.

Why and what is the challenge to Climate Tech? Something has been circulating and rumbling in the background, even before the US anti-climate tsunami of the first EOs hit.

Such movements can just start with a simple throwaway comment - someone posts this 👇 and it's all up in the air. 🤷♂️

Tommy is an investor, people listen. Things on X get amplified - point of reference, the state of the USA at the moment!

Why is it potentially dead as a 'brand' now - it has been through various iterations to suit market sentiment and parlance through history. Green Tech goes back as far as you would like to consider, and Sustainability was core to the survival and progression of society for hundreds of years. It was actually a thing, before it was a thing!

Clean Tech [a retrospective from 2013 here] was born out of a new investment class of the 1990s, with a wider focus on sustainability and environmental best practices. More recently, Climate Tech has been defined by the pressing need and specifics of CO2 reduction and climate change mitigation:

Climate tech is directly focused on technologies that reduce CO2 emissions, while cleantech includes a wider variety of technologies designed for environmental purposes.

An earlier article from me, as a reminder that whatever the name and brand, it all counts, which is why Konfab keeps a broad brief - we need a wide scope of systems thinking to deliver a multi-faceted approach across all the 'techs’, whatever they are called!

What's the Problem?

Well, since Tommy rolled the dice, the US has doubled down on 'drill baby drill' and additionally dismantled years of climate policy and environmental regulation, all in approximately 3 months.

On that note, if you want to take a deeper dive into why 'drill baby drill' won't happen, as he might hope, I can highly recommend these articles from researcher and journalist Justin Mikulka:

▶️ Oil & Gas Export Dellusions

Big Oil is far too worried about leveraging profits out to shareholders ASAP and exiting before they get stuck with liabilities and the clean-up bill for literally millions of wells.

Fascinating to read more about the inner workings of US Oil & Gas. Putting all that 'drill baby drill' bluster to one side, let's get back on track with Climate Tech.

The US as the 'big tough guy' 🙄 is the perceived leader of Climate Tech investment, and even before the chaos, 2024 saw a downturn from 2023, CTVC / Sightline Climate;

Climate tech funding fell 14%, contrary to optimistic predictions. The macroeconomic pressures of high interest rates, delayed IRA funding rollouts, and geopolitical uncertainties created significant headwinds. The "wait-and-see" investor crowd from 2023 held back, stalling the anticipated restart in 2024

Has the Teflon Don hit the final nail in the coffin then? 🤔

Perception and Deception

Climate Tech is perhaps its own worst enemy. Does the definition suggest a panacea, promising to solve the world's problems with a major technological innovation and fix 'climate'?

It's just a descriptor for an investment class after all. For many sensible and knowledgeable people, some climate technologies are an over-reach, a subsidy grab or an investor hail-mary. Promising the world, while delivering little. Yes, there is always investment risk and failure rate in technology development, typically 90% + in this sector.

But in the worst cases, are such technologies a distraction and delay tactic to ensure Business As Usual? There are some common culprits - here's looking at you Direct Air Capture, Carbon Capture and of course Hydrogen, plus many others.

We aren't getting into technology merits here today, but you can dig in further via the links. IEA Hydrogen 2023 Review:

Only 4% of this potential production has at least taken a final investment decision (FID)...27 Mt are based on electrolysis and low-emission electricity and 10 Mt on fossil fuels with carbon capture, utilisation and storage.

We have approximately 95Mt of Black Hydrogen derived from fossil fuels to clean up and replace with Green Hydrogen - it is part of the transition when used in the right places.

The VC investment still keeps flowing in though - in 2024 according to Crunchbase:

23 x hydrogen-focused startups globally have secured financing so far this year, bringing in over $1.4 billion in equity funding

Even during the process of writing this, another hydrogen bubble has popped, of the Nikola kind, which has a whole travesty of misdirection, misinformation and legal issues throughout its journey.

The landscape is filled with the rotting hulk of many a failed startup gone pop. Even a logical solid bet in European battery tech production via Northvolt, couldn't hang on.

Climate Tech startup failures and collapsed projects create a bad rep - but hey, that's the nature of innovation and VC investment! If only that were the whole story - the key issue with such technology solution wrong-turns, is they suck up publically funded subsidies, engineering resources, and most critically, time - they are a distraction we don't have the headroom for.

In many cases, the science is established and techno-economic engineering analysis can quickly clarify likely viability before any serious deeper analysis is undertaken.

It appears on the surface, in the historical VC Climate Tech feeding frenzy, not quite as much technical pre-screening and due diligence gets completed, as it once did.

Climate Tech Investment Cold Feet?

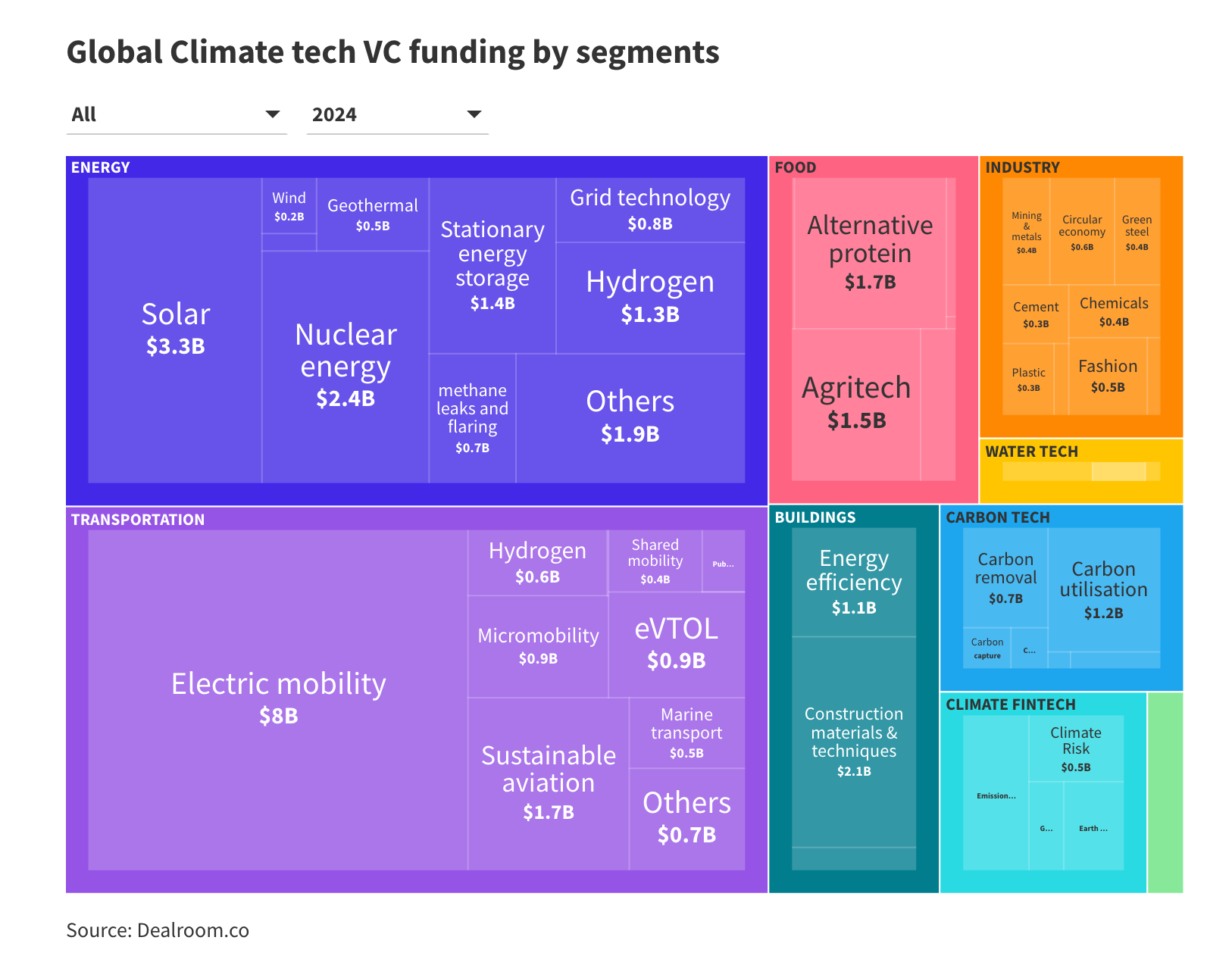

Not to worry, there is still plenty of money going in, as per dealroom segmented VC investment for 2024;

The other aspect to consider is that finance and investment are transitioning. We have many of the technologies and solutions in hand, they are now being deployed at scale globally.

2024 was a year of hunkering down – shoring up balance sheets, managing opex and getting ‘fit’ for more sustainable growth.” - Lila Preston, Head of Growth Equity, Generation

In 2024, awareness of the “missing middle” of capital became more pronounced as the climate tech industry continued to mature.” - Jeff Johnson, General Partner & Head of Climate, B Capital

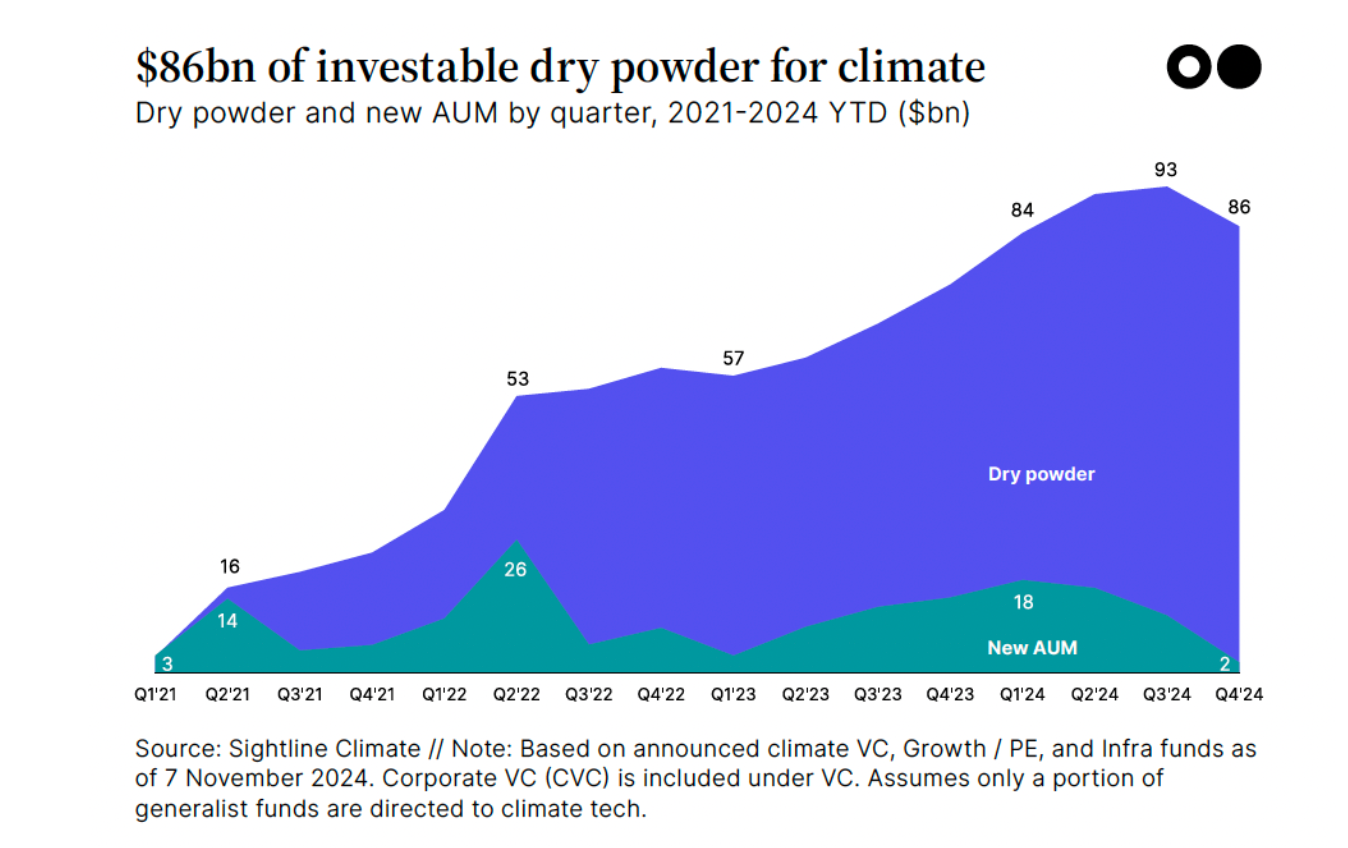

There is plenty more in the kitty - approx $86bn in investable dry powder across VC (including Corporate VC), Growth Equity / PE, and Infrastructure:

Expect to see a much broader mix of capital through 2025 - more growth equity and PE, later stage investments, project funding and infrastructure finance, plus banking and insurance. It's all in there as the market shifts to deployment and scale, from early-stage venture.

What Does Work Then?

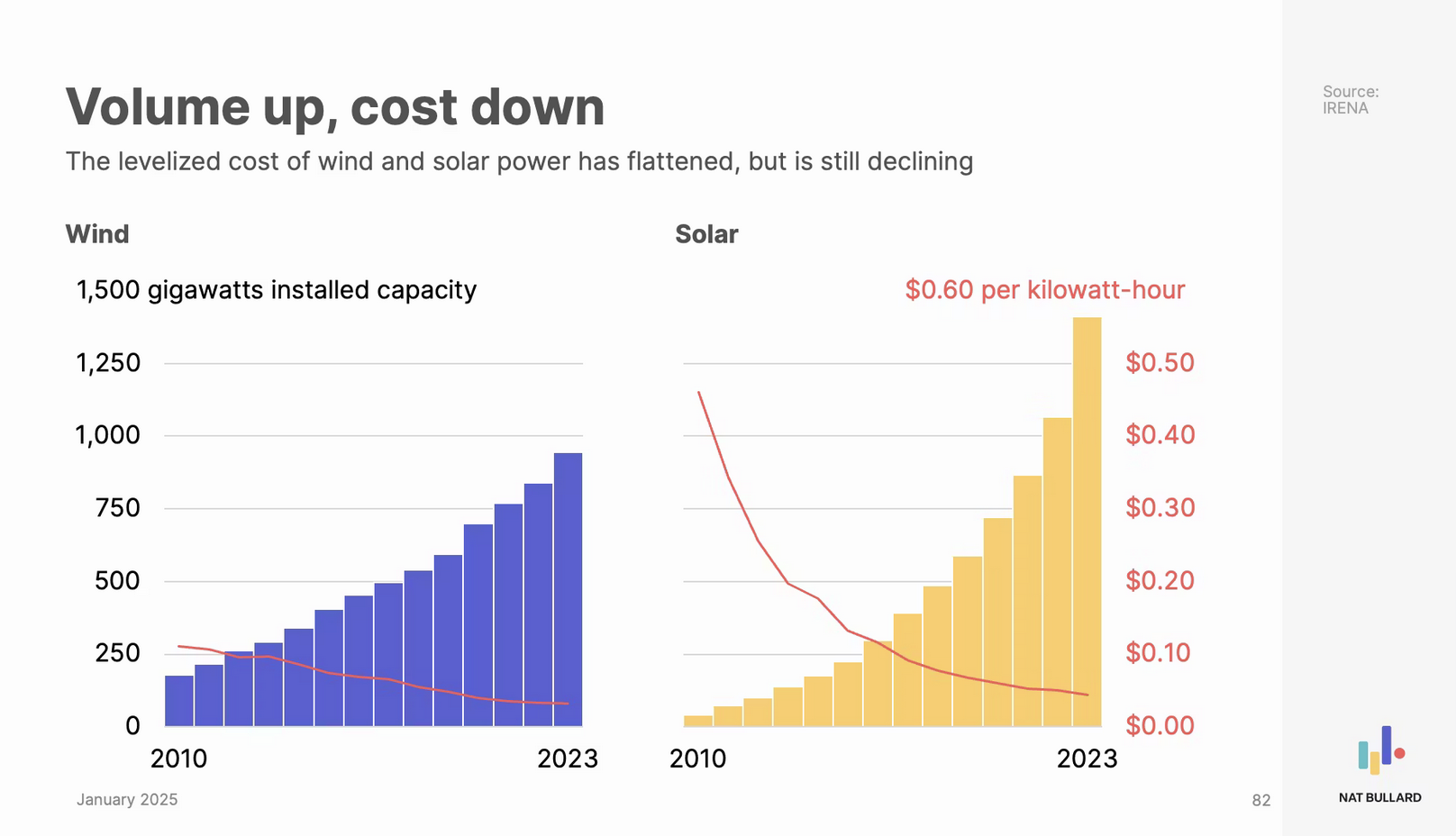

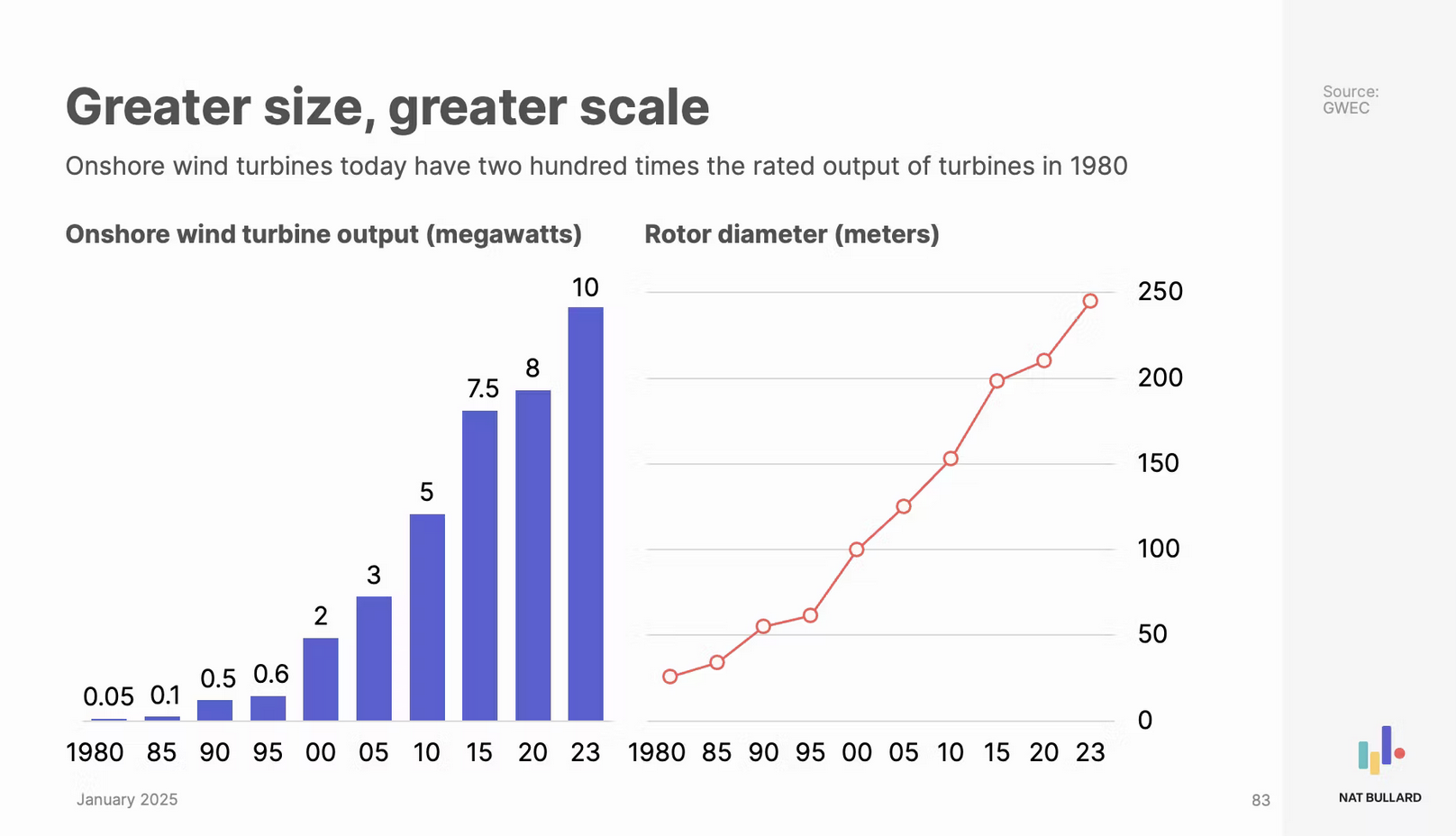

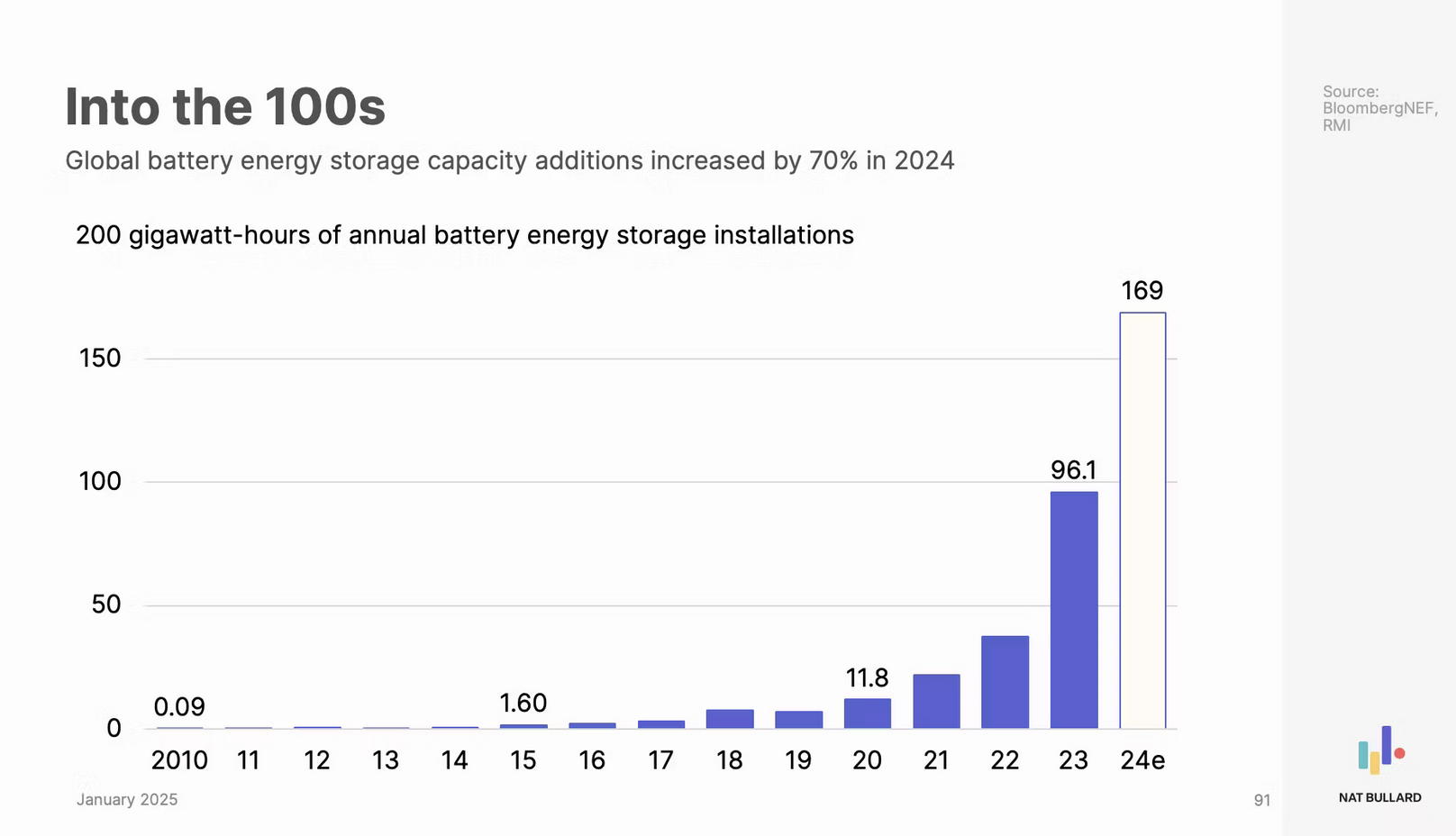

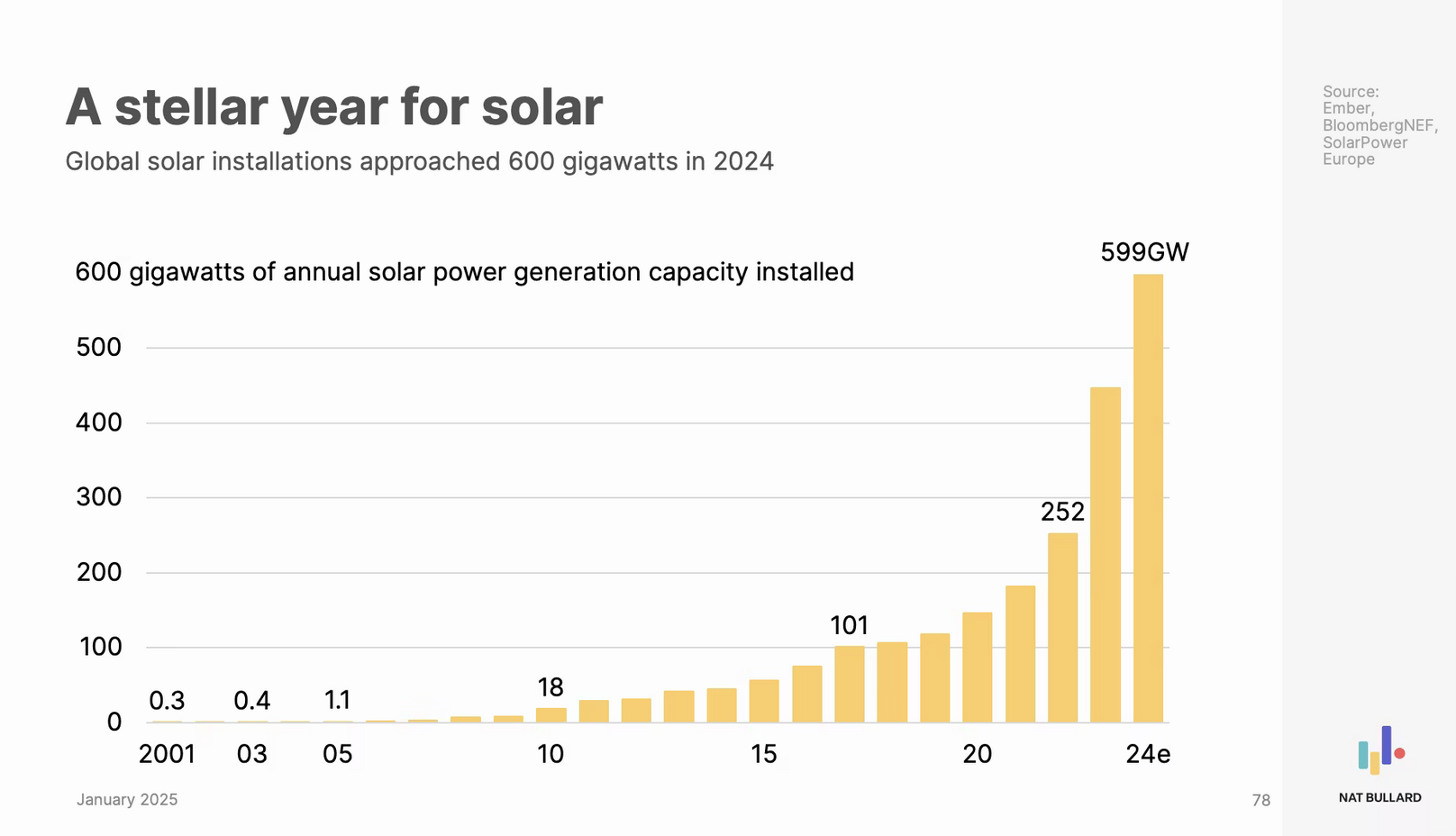

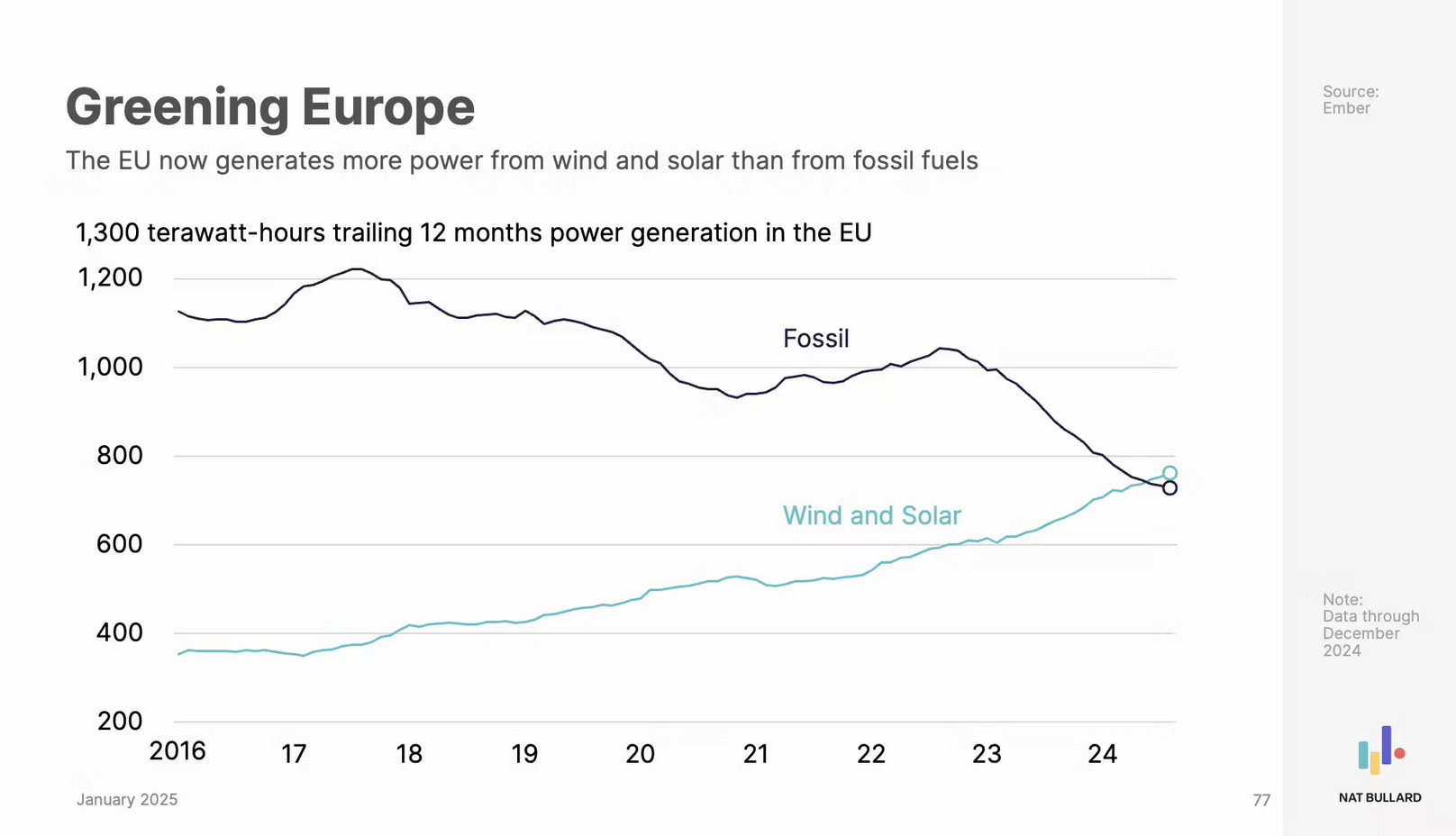

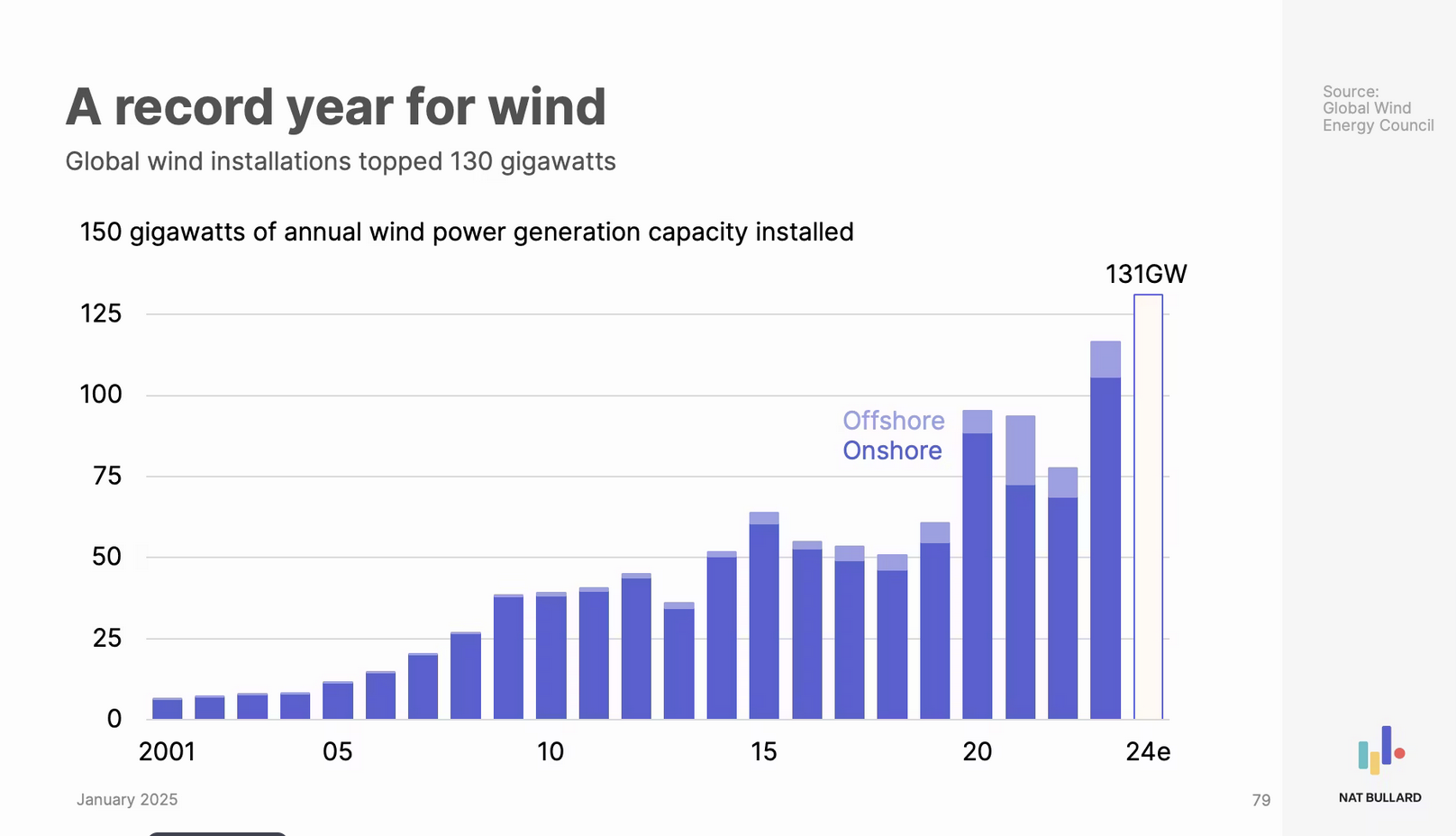

We should take a moment to recognise that deployment is happening, rapidly and at scale. We know China marches on at a pace that no one can match. In broader technology deployment, take a look at these global summary indicators from Nat Bullard:

Solar, Wind and Battery storage have all reached new records for growth, and continue to show cost reductions. Similarly, we march on with EV - Chinese EV maker BYD took a giant leap to world domination last year, with 29% growth, topping $100 billion in sales for the first time, shifting 4.29 million units.

As a comparison, Tesla, 1.79 million, and VW Group, 0.75 million. In 2025, the global market is expected to hit 20 million units, in comparison to 2024, care of Rho Motion;

🌏 Global: over 20 million, +18%

🇨🇳 China: 12.9 million, +17%

🇪🇺 EU & EFTA & UK: 3.5 million, +15%

🇺🇸 🇨🇦 USA & Canada: 2.1 million, +16%

This is good news - we have maturing markets, global trends and momentum. Nothing that happens in the US can change this. The rest of the world continues to grow through new clean / climate / net zero industries, the energy transition, and now with the additional reshoring of defence procurement. The US will fall further behind as it recedes into recession, hamstrung by attachment to Oil & Gas, and an economic strategy born of its esteemed leader who seems to be shunning all norms.

Energy Security and Defence

There really are no upsides to Trumpism, whether it is democracy, climate, economics, health, Ukraine, eggs etc. - well aside from Mother Russia's perspective.

However, one ray of light in all this chaos and geopolitical realignment, is energy security and defence are now more on the menu than ever before. Bad news of course by definition - people are dying, the lines are being drawn and redrawn in Europe - defence spending is about to take a mighty leap in every country's ratio of GDP.

Most of that will now of course be diverted away from the US, looking at you F-35 and the new F-47 [the narcissism!] whose order book is taking a major hit from former 'partners', plus all the other kit that once poured out of the US military-industrial complex. That's not coming back anytime soon.

No country wants to continue to be tied to global impacts on LNG prices. Additional gas import costs over and above the norm for the UK have surpassed £90billion since the invasion of Ukraine!

The global pathway to electrification is set, and grid investment and development is a key enabler. Grids are critical infrastructure, now even more so - they just got a timely boost. Sovereign energy resources, solar, wind, and hydro, will flourish in ratios depending on your geography. The decarbonisation of heating and cooling through geothermal is reaching it's time to shine.

The growth of interconnected grids in Europe will continue at pace, expect more HVDC, with robust protection for inter-country balancing and resilience. It will make for a stronger Europe, less reliant on LNG volatility. There might even be a 6GW trans-Atlantic HVDC from Canada across to Ireland in the next few years.

And it's not only energy - defence now is an umbrella cover for heightened focus on all aspects of infrastructure and food, water, transport, supply chain etc. The best part - all these things are improved through low-carbon, sustainable and 'Climate Tech' related solutions. 😱

Because they can, and have to be, managed better - with digitisation and monitoring, digital twin predictive modelling, risk strategies, efficiency, cost-effectiveness, resilience, and openness to innovation - all with enhanced sovereignty and strong partnership supply chain focus.

When you join the dots between climate, resilience, defence, and then growth, the picture becomes even clearer. There aren't many levers left for stagnant economies to pull, but Clean Tech, Climate Tech and Net Zero, whatever you want to call it, offer a big lever that is working - the next industrial age is here, and it's also much lower cost than we might have expected.

The Financial Times thinks Europe has the opportunity to jump into the void the US has left behind - I agree.

In the UK the Climate Change Committee recently reported;

💰 Net cost of net-zero 73% < forecast

✅ Total cost to 2050 = £108bn

✅ To 2050 is £4bn/yr which is just 0.2% GDP

📉 Household energy/fuel bills to fall £1,400

The CBI report supplements this;

📈 The Net Zero economy grew by 10% in 2024 [out performing all other sectors]

➕ Generated £83bn in gross value added (GVA)

This meme is an old classic meant for a different purpose, but it resonates well for the new world order, just as it did for climate science versus climate deniers.

Couldn't happen could it...or could it 💡

Climate Tech's New Clothes

Is Climate Tech dead then? No, not for as long as we need it. It might be to Tommy or some other unfortunate resident VC in the USA, but not to the rest of the world.

Climate Tech is moving into new territory, into deployment globally for some maturing technologies, and into more emission reduction enablers in the next few years.

Climate Tech has also got itself a new disguise, soon it will merge into a daily part of our lives through commercial and public channels, via innovation, resilience and planning, as part of our sovereign defence strategies.

The reality is that climate change science is unequivocal and undeniable, unless you are an actual denier. It offers better lifestyles, outcomes, and a liveable future, for people and the planet - at a lower cost than incumbent systems and solutions.

It is becoming THE choice, not A choice - it might be through the back door in disguise via an unexpected route, rather than welcomed in as the saviour - but I will take that any day!

You can say it is dead, delete it, remove it, defund and deny it, but as THE choice, ultimately the markets, people and planet will ensure it thrives.

It was a pleasure to attend and support the Chatham House Climate & Energy Summit recently - during the TeX Factor panel, friend of Konfab and panel moderator, Richard Delevan of Wicked Problems Podcast, asked Fiona Harvey, Environmental Editor of The Guardian, about Climate Tech....

I agree - Climate Change and Climate Tech are inescapable realities!